Innovation Is Accelerating Commoditization

Authored by Jonathan Needell, President and Chief Investment Officer May 31, 2021 Innovation is a funny thing. The word...

August 25, 2021

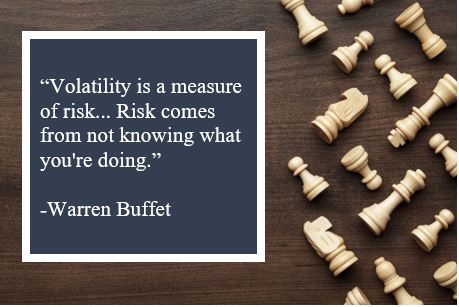

As John Paul Jones memorably put it, “It seems to be a law of nature, inflexible and inexorable, that those who will not risk cannot win.” Risk is an inextricable, unavoidable component of every investment decision, so when evaluating risk, it’s important to have a useful, consistent method of measuring it.

In the investment world, volatility, which measures the price swings of a given security or investment, is a common measure of risk. You may also have heard of beta, which purports to measure the amount of systematic risk an individual security (or other investment) has relative to the overall market. A beta of 1 indicates a perfect correlation to the overall market (just as “risky” as the overall market), while a beta of less than one translates into less of a correlation (and, the thinking goes, less risk). A beta of 2 would mean that a given investment experiences twice the price volatility of the overall market, and is, according to conventional investment wisdom, twice as risky.

As useful as these metrics can be, it’s important to note their limitations. For starters, using price volatility or beta as stand-ins for risk ignores the fact that when an investment declines in value, the investor is under no obligation to sell it and realize that loss. Picture an investment with a high degree of price volatility, which fluctuates wildly relative to the market. If the investment whipsaws downward by 20%, the investor need not immediately pull the trigger and sell, realizing the loss—depending on their individual investment goals, they may hang onto the investment for as long as they like. If the investment is quite volatile, it can just as easily whipsaw back upward, canceling out the loss, which in any case is unrealized if and until the investor sells.

Additionally, using volatility as a stand-in for risk ignores the entry point for an investment. If an investor acquires an investment at a low price, then the subsequent price swings may not matter so much, nor translate into additional risk of loss for that investor, so long as those price swings don’t bring the value of the investment below the investor’s entry point. Price volatility also tends to ignore the cashflows which an investment can provide to an investor during the hold period. In the overall market, these cashflows (typically in the form of dividends or interest payments) are often negligible relative to the price of a given security, but in the world of real estate, yields can be quite substantial. In some cases, particularly in real estate, even if an investment has declined somewhat in value, the cashflows it generates while an investor holds it can more than make up for a price decline.

If the investment entry point is low (making money on the buy) and cash flow significant, volatility should be of less consequence. So, risk is better understood through fundamental understanding of the price you are paying for an investment, the cash flow it produces, and the resiliency of both rather than the volatility of the price or value of the investment.

*The views and opinions expressed in this article are solely my own.

For questions, contact investor relations at investorreporting@kimc.com or 949-800-8500.

Back to All

Back to All

Authored by Jonathan Needell, President and Chief Investment Officer May 31, 2021 Innovation is a funny thing. The word...

Authored by Jonathan Needell, Associate Investment Director October 27, 2020 Investors of all stripes are frequently admonished to go...

Authored by Raymond Hu, Senior Investment Director – Head of Real Estate Credit May 2, 2023 Commercial real estate...

Seeking Investment Stability During a Recession Authored by Trevor Schuesler, CFA, Associate Investment Director February 22, 2021 Since the...

The Affordable Housing Crisis The U.S. is currently undergoing a major housing crisis with only 37 affordable rentals available...

By Heather Lewis, Chief Compliance Officer and Jeanna Mackin, Associate Director of Human Resources August 9, 2023 Over the...

Authored by Jonathan Needell, President and Chief Investment Officer April 30, 2021 Commercial real estate’s various sectors always have...

Authored by Jonathan Needell, President and Chief Investment Officer August 19, 2021 (reposted from LinkedIn article published on October...

18101 Von Karman, Suite 1100

Irvine, CA 92612

(949) 709-8888

(949) 800-8500

investorreporting@kimc.com

Copyright © 2024 Kairos Investment Management Company | Disclosures