Esusu: A Case Study in Optimizing Social Impact Programs

Authored by Anita Rodriguez, Impact Program Director November 11, 2022 Resident social impact programs can be an excellent way...

By Raymond Hu, Senior Investment Director – Head of Real Estate Credit

October 10, 2023

Not so long ago, near-zero interest rates and plenty of capital meant that traditional lenders—think larger national banks—were incentivized to offer debt to commercial real estate developments and investments. Thanks to this, the cost of capital was very low. This was the era of “cheap money.”

What a difference a few years make.

In normal markets, the so called “wall of maturities” can be accommodated by traditional financing methods. When lenders drop out of the market or tighten up lending standards, that “wall of maturities” creates a scarcity of capital.

That is exactly what is occurring:

It’s true that regional banks stepped in to take up some of that slack that the larger banks left behind during the COVID-19 pandemic. However, the market just lost three of the largest regional banks in the first half of 2023 which means both borrowers and depositors remain nervous about the current role of small and mid-size banks. The lack of liquidity from both large and regional banks has caused a credit crunch in the market.

With traditional lenders sitting on the sideline, what debt is currently in demand and available? The answer is that more real estate developers and investors are seeking shorter-term debt issued by private debt funds.

The Offerings

Traditional lenders issue loans based on in-house deposits, and they must maintain a certain amount of reserves as required by federal regulators. The fewer deposits, the less debt available. Private debt funds operate differently. They raise money from investors, then lend that money to real estate owners and developers with more flexibility and creative and customized structures. There’s no debt-to-capital ratio regulations and reserve requirements, as there are with traditional lenders. We believe through private debt funds, borrowers obtain liquidity, while investors can achieve healthy returns.

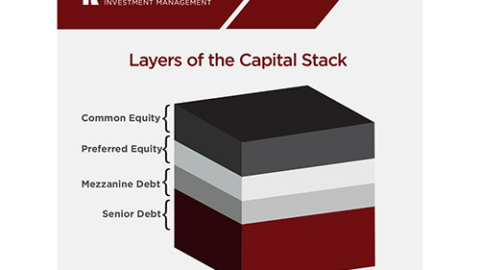

More of today’s commercial real estate borrowers are applying for bridge loans or mezzanine loans. These loan types are similar; in fact, a mezzanine loan is a type of bridge loan. While bridge loans are backed by property or other assets, mezzanine loans rely on a borrower’s equity as collateral.

These debt types offer the following benefits:

Shorter terms. Mezzanine and bridge loans are short-term, ranging from one to three years. After this, the borrower can refinance into a longer-term, lower-interest loan. In many cases, there are no prepayment penalties for early payoff. Additionally, interest on the loans is tax deductible. While there seems to always be a reason to borrow short or use bridge financing it is specifically in demand today. Given the current credit crunch it is logical that the demand for shorter term loans is higher than normal as owners only want to rely on this market until a healthier debt market exists.

More flexibility. Because private debt funds aren’t bound by the same federal and state regulations as their traditional lending counterparts, mezzanine or bridge funding can be tailored to a borrower’s specific situation and needs. Mezzanine and bridge loans also have shorter underwriting and approval periods, meaning a faster path to the liquidity provided by these loans.

The Forecast

The outlook on traditional lending for commercial real estate is murky. Billions in debt maturities are coming due. Meanwhile, inflation continues to impact cash flow and valuations, which means that traditional lenders face possible loan defaults.

Larger traditional lenders are continuing to circle the wagons. Even if the cost of borrowing were to decrease, the national and regional banks still implement stringent underwriting requirements for borrowers. They’ll also remain extremely selective when it comes to financing commercial real estate projects, and often limit proceeds, requiring additional capital from other sources to bridge the gap.

When encountering volatile periods like this, the real estate equity market is expected to take longer to adjust than the debt market. The debt market is moving more quickly and there will be many interesting opportunities for private debt funds which have the capital for deployment and are flexible investing across the capital stack. These lenders are also in the process of actively raising more money. We believe that these loans are proving to offer equity-like returns in a secured debt position to investors in today’s environment.

Because of their flexibility, less stringent requirements, and shorter-term commitments, it’s anticipated that the demand for bridge and mezzanine loans will continue. While the capital markets remain volatile and uncertain, these non-traditional lenders are in place to provide liquidity. This, in turn, will ensure ongoing investments in, and development of, commercial real estate projects.

For questions, contact investor relations at investorreporting@kimc.com or 949-800-8500.

Back to All

Back to All

Authored by Anita Rodriguez, Impact Program Director November 11, 2022 Resident social impact programs can be an excellent way...

Authored by Jonathan Needell, President & Chief Investment Officer August 28, 2020 In the United States, the ongoing COVID-19...

By Justin Salvato, Senior Partner at Kairos Investment Management Company October 23, 2023 Not long ago, capital deployment was...

Authored by Jonathan Needell, President and Chief Investment Officer June 6, 2022 Environmental, social and governance (ESG) has become...

Authored by Jonathan Needell, President and Chief Investment Officer November 7, 2022 Affordable housing, defined as housing that a...

By Jonathan Needell, President & Chief Investment Officer July 27, 2023 Kairos recently made the move to a new...

Authored by Jonathan Needell, President and Chief Investment Officer August 25, 2021 As John Paul Jones memorably put it,...

Thoughts on the Economic Ramifictions of the COVID-19 Pandemic Authored by Jonathan Needell, President & Chief Investment Officer July...

18101 Von Karman, Suite 1100

Irvine, CA 92612

(949) 709-8888

(949) 800-8500

investorreporting@kimc.com

Copyright © 2024 Kairos Investment Management Company | Disclosures